The Creeping, Crawling Financial Crisis

October 28, 2025

Health Savings Accounts — the Triple Tax Threat!

March 10, 2026

By Clark Troy

Those close to retirement can afford neither to fall asleep at the wheel or rush to the illusory safety of cash

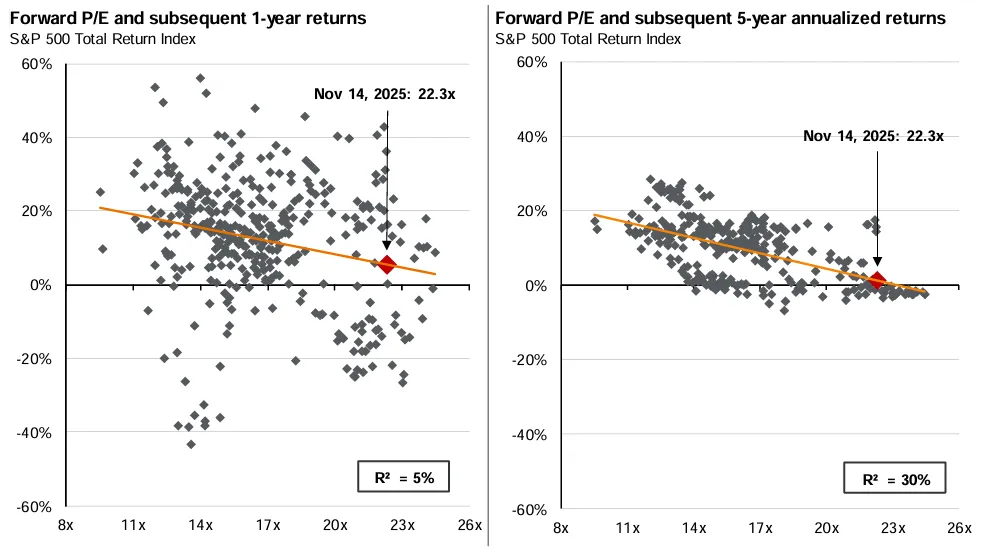

There’s a lot of chatter out there about where we are in the AI hype- and market-cycle. Many bandy about the word bubble when babbling of big beneficiaries of AI bets. Without a doubt, stocks are priced at a substantial premiun. The forward-looking price-to-earnings ratio (PE) for the S&P 500 is 22.3, well above its historical norm of 16.8. For the top 10 stocks — which contain all the headline names for which the world is so giddy and which comprise a near-record 40.9% of the index’s value — forward PE is 29.1 vs. an average of 20.7.

That was a lot of numbers. The main thing is that stocks are currently valued highly by historical standards, and these kind of numbers tend to be mean-reverting over time. Which could happen one of two ways or some combination thereof. Companies’ earnings could go up or their stock prices could come down.

For now stocks keep going up and up — though we’ve had some down days in the last couple of weeks. It’s easy to get caught up in the hubbub and want to pile on risk.

Another thing that’s happening is that affluent people are starting to think about retiring earlier. I know people who’ve done it and others who are contemplating it. Fattened portfolios, generalized ennui from years of the pandemic and its aftermath, and our eternally fractious and combative political environment are leading many to just wish to hang it up and get on with enjoying life.

Most of us are also going to live a long time. The average life expectancy for a 60-year old American male is 82, for women it’s 85. But — and this will surprise no one — longevity statistics are further skewed by income. Americans in the top income decile at age forty have life expectancies of 85 for men and 87 for women.

So those thinking of retiring early need to think seriously about question of whether they have enough money to live as they’d like to live for a pretty long time. This thought process is complicated by the problem of sequence of returns risk. Put succinctly, if markets go down early in your retirement years, it can be hard to climb out of the hole they dig for you. If your portfolio falls by a third in the early years of your retirement but you don’t adjust your rate of spending, you erode your wealth pretty quickly.

There are a variety of ways to manage around sequence of returns risk. The easiest way is to just live cheaply and take pleasure in riches you’ve piled up around you in the form of books, friends, exercise routines, the simple pleasures of cooking good meals, and so on. If your expenses are low enough relative to your assets and cash flows (defined benefit pensions for the lucky few plus Social Security for the rest of us), you can ride out some bad years and not be concerned about risk.

But that’s not how most people think about retirement, and especially those who are thinking of retiring on the early side. Lots of them want to get out and do things while they’re young enough to do so. I get it.

But let’s return to the question of sequence of returns risk and the current moment. Are we in a bubble? Will the stock market, and particularly its highest flyers, get its comeuppance (or perhaps I should say “comedownance”)? Nobody knows for sure, but history says that it’s not unlikely. The scatter charts below — provided to us by JP Morgan Asset Management — show us the S&P 500’s historical range of total returns (price change plus dividends) over 1- and 5-year periods when it has been valued at various levels, with a pin stuck in where we are at time of writing. Looking out over one year, the market has had a range of experiences, some of them good, with a slightly denser cluster of quite bad outcomes. A five year time horizon, however, looks worse. Annualized returns are exclusively negative. The good news is that they’re not that negative, but remember, they’re annualized. Five years at -3% will reduce a portfolio’s value by 14%.

Source: JP Morgan Guide to the Markets

Of course, there’s no certainty. History never repeats itself exactly, but it often rhymes.

What to do?

Take some risk off the table and diversify. Don’t get lulled into a false sense of security by the market’s siren song. Be sure you have enough in something cash-like (money market fund, high-yield savings account, ultra-short term bonds) to fund your plans for a year or two. Bulk up your holdings of bonds as well as other asset classes (foreign stocks, REITs, etc).

Don’t stray too far from the workforce. Think about yourself as potentially taking a sabbatical rather than retiring. Stay in touch with your field and with former colleagues and be open to consulting opportunities as they present themselves.

Ponder other jobs you might enjoy doing at a lower rate of pay for a few years.

Remember that, if we do enter a bear market, historical evidence suggests that it will probably be a good time to be adding funds to a 401k or other retirement plan.

Be honest and realistic with yourself about your motivation for your spending. Are you spending money doing things you actually want to do, or on things you think you’re supposed to want to do?

The goal is not to have the most money when you retire, it’s to have enough money over the course of your retirement.

But you can’t just rush to the illusory comfort of cash either. Given current global sovereign debt levels, low birth rates and governments’ inability and unwillingness to tell retirees the hard truth that their benefits need to be trimmed — the coming decades will probably be marked by significant inflation as governments inflate away the real value of their liabilities. People will need to maintain higher levels of exposure to equity markets than was once thought prudent to maintain purchasing power. There will also be recessions and bear markets.

Unless AI just fixes everything for all of us. The world seems to be betting on that. It’s a big and risky bet.

This article originally appeared on Straight Edge Finance. Click here to read more from Clark Troy.

{kind=link}

{kind=link}