The Creeping, Crawling Financial Crisis

November 18, 2025

What they are, and what they aren't

By Clark Troy

The US Federal Tax code challenges the typical mortal through — among other things — the endless proliferation of account types and rules associated with them. 401k, 403b, 457f, 457b, defined benefit, cash balance, PSP, Roth IRA, Roth 401k, Solo 401k, SEP IRA, SIMPLE IRA, 529, Coverdell, Donor-Advised Account, FSA, HSA, and the good old brokerage account, to name some of the basic categories of account types that Americans may run across in the course of their working lives. Many of these, as will surprise few, come in varied shapes and colors. It’s a lot to take in. Many an hour can be frittered away in confused frustration. Others simply walk away.

But it pays to familiarize yourself with them. Today I bring to you the Health Savings Account, one of the more recently birthed of these animals, and one of the more confusing. Established at the end of 2003, Health Savings Accounts are available to the 40-50% of the privately-insured Americans who are enrolled in High Deductible Health Plans, HSAs are often confused with FSAs (Flexible Spending Accounts), which can offer the ability to put aside pre-tax money to defray various types of expenses — healthcare, childcare, parking and travel. FSAs, however, must be spent by the end of the calendar year or shortly thereafter. HSAs offer the ability to defer funds from year to year and therefore to invest for growth.

A big difference indeed, which gives rise to the HSAs much-ballyhooed “triple-tax benefit,” which for me for some reason invariably brings to mind the “triple guitar threat” of Canadian band April Wine, who by some strange accident of history was one of the few bands that had music videos around 1981 and therefore got into really heavy rotation in the early days of MTV. April Wine somehow never lived up to the I’m sure very genuine enthusiasms of VJs Martha Quinn and Mark Goodman. The HSA, well it’s the real deal.

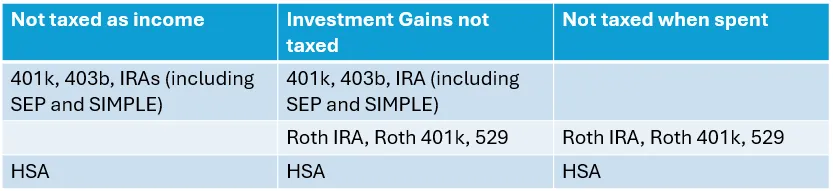

Alone amongst the firmament of IRS-defined account types, the HSA offers tax benefits at each moment of the income tax lifecycle. Contributions are deductible from income. Investments grow tax-free. If spent on qualified healthcare expenses, no taxes are due upon withdrawal. Let’s compare with a few of the most popular account types.

As we can see, the HSA is the champion here, the loan account type that offers entirely tax-free treatment of your dollar from cradle to grave. The key, counterintuitively, is to not spend the money on healthcare expenses in the year in which it was earned. Instead, the ideal thing to do is invest for growth and hold for a long time.

But how much money could one get into an HSA? Though not as generous as some of the other account types, HSAs offer the ability to shelter a non-trivial amount of cash $4400 for individuals or $8750 for a family of two or more, with a $1,000 catch up contribution available to those aged 55 and older. Assuming this amount stayed the same (it won’t, it will rise with inflation) and one earns a real return (i.e. net of inflation) of 4% while contributing $8750 to your HSA from the age 35 to age 65, you’ll end up with about $490k in today’s dollars. If you then let the money ride a further fifteen years until you’re 80, you’ll have about $884k of real purchasing power, i.e. 2026 dollars.

Now, you may well ask, why would I want to save so much money until I’m 80? The answer, I am sorry to tell you, is that you might need money to pay for long-term care costs when you’re older. Funding long-term care is the thorniest of all financial planning problems. Long-term care insurance is a bit of a mess. The first generation of long-term care policies were underwritten poorly as insurers failed to accurately project what costs would be like in the future. The hybrid life/long-term care policies prevalent today offer high costs and smoke and mirrors to make them look more attractive than they really are. It ends up being quite expensive to buy a material amount of coverage.

As you age, HSAs offer some good news and some bad news. The good news is that, if you don’t end up needing to use the money for healthcare purposes, after age 65 you can take the money out for any purpose and it’s taxed as ordinary income, just like money that goes into your 401k or 403b. So an HSA can act to some extent as an extension to your retirement plan and, given that HSAs offer the absolute best tax treatment of all tax deferment plans, it might even make sense to contribute the maximum to an HSA even if it means you can’t contribute the maximum to your 401k. So long as the investment options available to an HSA are similar to those in the 401k, the additional optionality upon distribution offered by money in an HSA make it a better bet than money in a 401k.

The bad news is that HSA’s taxation regime at death treatment is suboptimal. For a married couple, HSA money is available for the needs of either. When the second spouse dies, the entire balance in an HSA is a treated as a lump sum for their heirs, so it ends up being taxed at the heirs top marginal rate and can easily drive them into a higher bracket. HSAs don’t even have the 10-year distribution treatment now available to an Inherited IRA. One caveat here: over time lobbying pressure by the financial industry tends to work these kinds of issues out with the IRS. I would bet that twenty years from now Inherited HSAs will offer tax treatment similar to Inherited IRAs, though unless the deficit can be brought under control which will negatively impact projected tax revenues (as an improved Inherited HSA tax treatment would) will have a battle to fight in Congress.

One thing which I only just learned is that HSAs are available to self-employed people who don’t have employer-provided healthcare, but instead get plans through the Obamacare exchange. You can open an investment account at any of the large discount brokerages (Schwab, Fidelity, Vanguard) who partner with other firms that provide record-keeping and tax reporting. Google it. It’s not rocket science, though it does require some follow through to get accounts set up and funded.

One last last thing: HSAs are a fine thing, but they are no wholesale replacement for health insurance. Various proposals from the Trump administration and other members of the Republican caucus seek to turn HSAs into the primary vehicles through which many Americans fund their healthcare needs. Anyone whose had a family member go through cancer treatment or some other major healthcare event will know that it’s very hard to save the types of sums one needs to pay for treatment in America, as currently priced. Absent major reform in healthcare pricing and provision, the idea of HSAs as a primary funding mechanism for Americans’ healthcare needs is the very reddest of herrings.

This article originally appeared on Straight Edge Finance. Click here to read more from Clark Troy.

{kind=link}

{kind=link}

{kind=link}