I’m not wealthy

July 17, 2025

The Interest Rates We Really Want

August 26, 2025

By Clark Troy

Let’s try a little thought experiment. When is it most important to save on taxes? As well-trained consumers, our initial inclination may be to say “now” or “this year.” So many of us view a rebate check from Uncle Sam each April as a sign that we’ve done and planned well.

But as we proceed in life, gaining financial footing and becoming able to think about ever longer periods of time, extending our horizon from the pay period and where’s the party this weekend to years and specific goals to decades and beyond, it makes sense to incorporate the same way of thinking into tax planning. Really, what we want to think about is not how much we pay in taxes this year but how much we pay over the complete arc of our lives and, if we plan well, how much our children pay on assets we bequeath to them.

The juncture where most Americans have to develop this habit of thinking comes when we have to choose how we would like to contribute to 401k or 403b retirement plans which comprise the foundations of our retirement planning. Should we put money into them on the traditional pre-tax basis, which reduces our present income but obliges us to pay ordinary income taxes in retirement, or on a Roth basis, in which we pay taxes on income now but never again in the lifetime of the wage-earner or their spouse (or the first ten years after the second-to-die spouse passes away, if the retirement assets are inherited by children)? The question is exactly the same when deciding between contributions to traditional or Roth IRAs, and is similar but enhanced when pondering whether to convert funds in pre-tax IRAs into Roth assets.

Let’s look at the basic math. It all depends upon your the relationship between your current tax rate and your future tax rate. If your taxes will be lower in the future, it makes sense to take money out of today’s paycheck and pay the taxes in the future. If your taxes will be higher in the future, it makes sense to pay taxes now and contribute to your retirement plan or IRA using the Roth option.

That’s why the standard thinking has trended towards having people early in their career use make Roth contributions early in their careers, when their salaries were lower, and then switch over to pre-tax contributions around the age of thirty as their salaries rose, pushing them into higher tax brackets. Then, when they retired and their incomes dropped, it has often made sense for those with large retirement plan balances to convert pre-tax assets into Roth assets by doing “Roth conversions,” which basically means taking distributions from IRAs up to the edge of the 22% or maybe 24% tax bracket to get taxes paid on assets now.

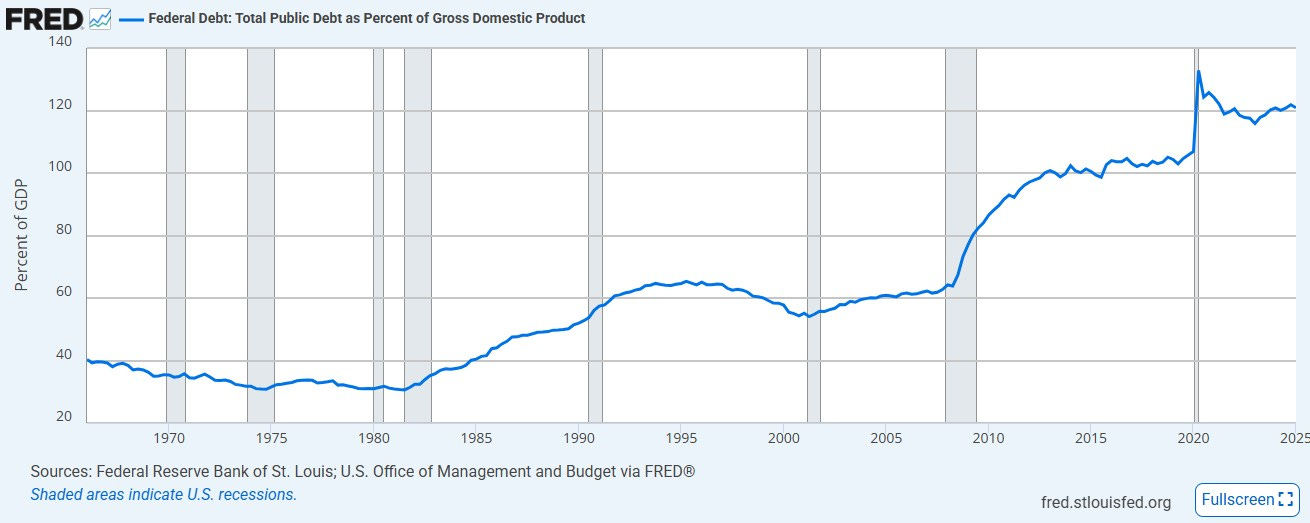

But, as we know, no matter whose lips we read, today’s tax rates may well not be tomorrow’s, so we need to think about more than just the micro dimension of our own household income when forecasting what our current tax rates will be. We also need to think about the macro side of things: what will US tax rates as a whole look like? The chart below shows the ratio of the US Total Public Debt to US GDP. People started making a fuss about the debt back during Reagan’s years, installing the first National Debt Clock near Times Square in 1989. Over time the debt grew higher, then higher still during and following the financial crisis of 2008-9, then rocketed to stratospheric levels during and following COVID. The Biden adminstration made only incremental progress towards reducing it, and the recently passed OBBBA promises to extend large annual deficits out into the future, adding an additional $4-$5 trillion to the national debt over the next decade.

All this bodes poorly for future tax rates, particularly as interest rates will likely never be as low as they were in the decade following the financial crisis, so the cost of servicing the US debt will be higher in the future. It is therefore rational to think that taxes will be higher in the future, which argues for going ahead and paying them sooner rather than later. Most of the CPAs and tax people I know, regardless of party affiliation, advocate for judicious, planned use of Roth conversion strategies.

On the subject of future tax rates, one more variable has to be considered: who will be paying the taxes? Thus far we’ve been discussing about a wage-earner or their spouse. But what if they each pass away and bequeath pre-tax IRA assets to a child? Time was, before the 2019 SECURE Act, the next generation could take advantage of the so-called “Stretch IRA” and take Required Minimum Distributions from the IRA based on their own life expectancy. In the case of all but the largest IRAs, the distributions, would typically not be large enough to impact the heir’s tax bracket.

The SECURE Act changed that. Now, most next-generation heirs of IRA assets must empty inherited IRAs within 10 years of their parent’s death. If a parent dies at, say, 80 and had their child at the age of 30, the child would be 50, in peak earning years. Now if the child inherits a $500k IRA that has to be emptied in 10 years, all of a sudden we’re talking about sums that could impact their tax bracket. So there’s that to think about. But not if the money’s in a Roth IRA. An Inherited IRA still has to be emptied at the end of 10 years, but none of it impacts the inheritor’s taxable income.

OBBBA added another wrinkle to this thinking. On the campaign trail President Trump had pledged to make Social Security tax free. To actually craft legislation that could pass muster with more fiscally conservative factions within the Republican Party, the bill actually adds a $6,000 per person deduction from income for persons over 65, which stacks on top of the standard deduction and the pre-existing $1600 per person senior deduction to give married couples the ability to deduct $45,200 a year. For the purposes of this article, the key point is that the $6k per person deduction phases out for those filing jointly between at between $150k and $250k in income (or between $75k and $175k for those filing individually).

Bearing in mind the numbers of Americans mentioned in my prior post as having $2-$5 million in assets and up, many of whom may expect Social Security income of $70k-$80k range (before allowing for the broadly expected 20-25% adjustment to benefits expected around 2032-3 which may be borne disproportionately by this segment of the population), there are a lot of people who may want to think about limiting their income in retirement and preserve as much of this deduction as possible by converting more pre-tax IRA assets to Roth ones.

One caveat is in order. Because of the budget impact of the $6k senior deduction, the OBBBA legislates it into being only for the years 2025-2028. Thereafter it has to be voted on again, where it will be buffeted between the Scylla of fiscal reality and the Charybdis of the rapacious and very active retiree voting segment. In 2028 the oldest Boomers will be 82, the youngest 64. Who will bet that either Republicans or Democrats will campaign on taking away this generous deduction, based on Bush the elder’s campaign experience back in ‘92 when he had challenged voters to read his lips but then he yielded to fiscal reality and raised taxes nonetheless?

But now we are deep in the weeds of forecasting and speculation, the second to last refuge of scoundrels. Let’s climb back out onto firmer ground.

When thinking about the Roth vs pre-tax retirement plan contribution questions, aside from the tax issue there’s an additional, more fundamental benefit. If you make Roth and pre-tax contributions of an equal amount, the Roth one will reduce your paycheck by more, because you’re paying taxes on the money too. So a $1,000 contribution to your Roth 401k at 20% withholding reduces your paycheck by $1,250, whereas as pre-tax contribution reduces it by $1,000.

If you reduce your current income by more and learn to live on less, you will be more easily satisfied in the future. That is the truest math of all.

This article originally appeared on Straight Edge Finance. Click here to read more from Clark Troy.

{kind=link}

{kind=link}